A 1031 exchange in Ohio lets you sell investment real estate and reinvest in like-kind property while deferring the tax on the gain. The federal rules apply the same way everywhere. Ohio has a low and falling state rate and no nonresident withholding step, and it is home to one of the largest industrial projects in the country right now. We act as your qualified intermediary, holding the proceeds and handling the documentation so the exchange holds from sale to closing.

Table of contents

- How much is capital gains tax on real estate in Ohio?

- Ohio 1031 exchange rules and timeline

- 1031 exchanges across Ohio markets

- Common Ohio 1031 exchange mistakes

- Start your Ohio 1031 exchange

- Frequently asked questions

How much is capital gains tax on real estate in Ohio?

Ohio taxes the gain as ordinary income at a rate of roughly 2.75% to 3.5% for 2026 as the state phases toward a flat 2.75%, with lower-income amounts exempt, so confirm the current figure. Some municipalities levy their own income tax, generally on earned income. The state rate sits on top of the federal tax an exchange also defers:

- Long-term capital gains at 0%, 15%, or 20%, with the 20% rate applying above $545,500 of taxable income for single filers and $613,700 for married couples filing jointly in 2026.

- The 3.8% Net Investment Income Tax above $200,000 of modified adjusted gross income for single filers, $250,000 for married couples.

- Depreciation recapture, taxed as unrecaptured Section 1250 gain at up to 25%.

- Ohio's rate on the gain.

Ohio conforms to Section 1031, so a properly structured exchange defers both the federal and the Ohio tax. The full federal framework is in our main 1031 exchange guide.

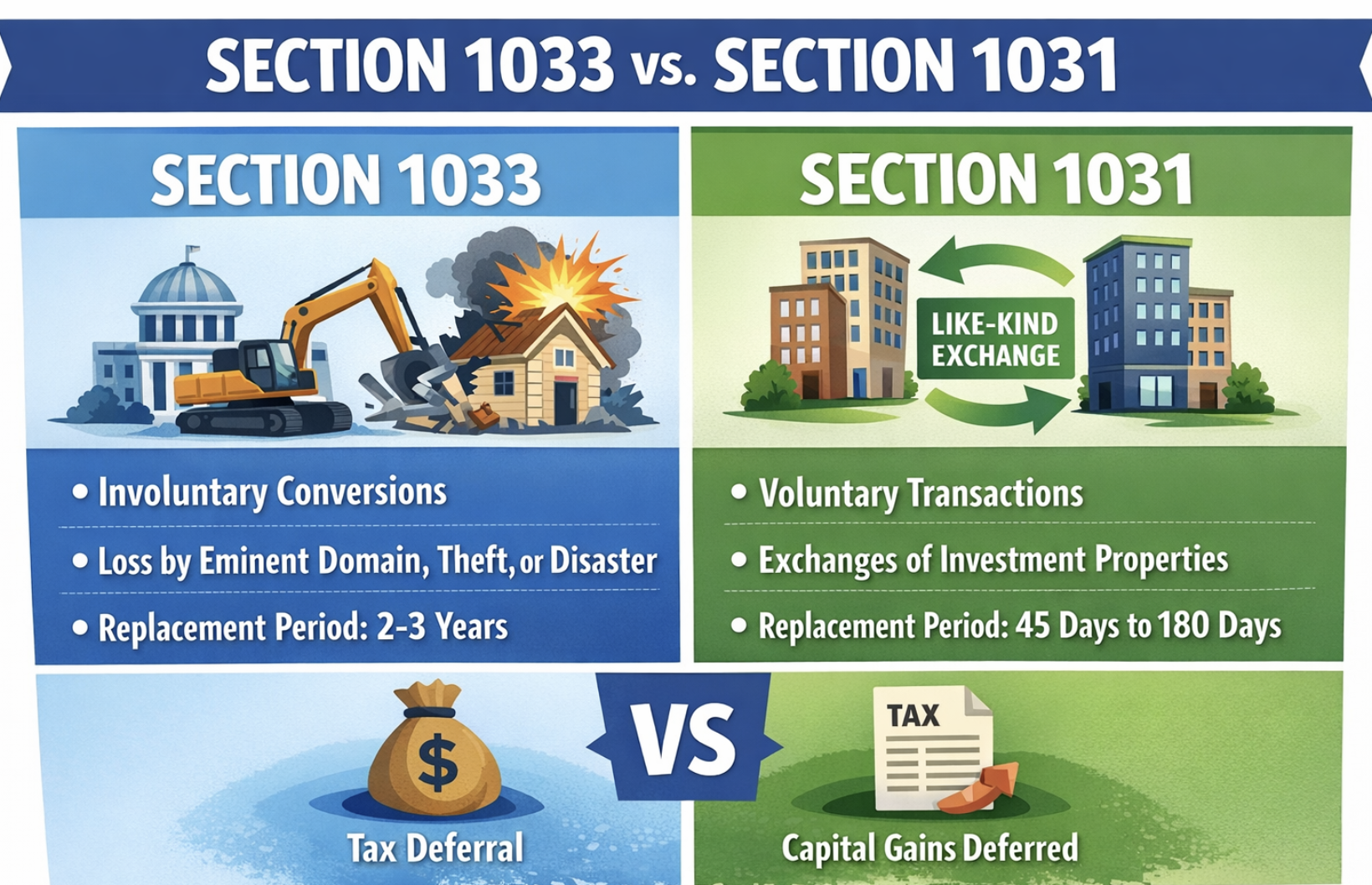

Ohio 1031 exchange rules and timeline

The federal deadlines govern, and they are strict:

- 45-day identification. Identify replacement property in writing within 45 days of the sale.

- 180-day closing. Close within 180 days of the sale, or by your return due date including extensions, whichever is earlier.

- No constructive receipt. Proceeds go to your qualified intermediary, never to you.

- Equal or greater value and debt. Reinvest all net proceeds and match or exceed the relinquished value and debt, or the shortfall is taxable boot.

- Same taxpayer. The entity that sold must be the entity that buys.

Ohio does not impose a general nonresident real estate withholding at closing, so closings here are straightforward.

1031 exchanges across Ohio markets

Columbus has been the state's standout growth market, the capital and a university and insurance center, and now the site of a major semiconductor manufacturing project nearby that has driven a wave of industrial, multifamily, and commercial demand and supplier development. Cleveland anchors the northeast with a strong medical sector, led by a world-renowned hospital system, plus multifamily and industrial property. Cincinnati in the southwest combines consumer-goods corporate strength with a logistics base tied to the air-cargo hub across the river, supporting industrial and multifamily exchanges. Dayton and Toledo add manufacturing and commercial demand. Ohio property tax is moderate to high and set locally, so confirm the rate for any replacement deal.

Common Ohio 1031 exchange mistakes

- Taking receipt of the proceeds, even briefly, which disqualifies the exchange.

- Missing the 45-day identification window.

- Trading down or pulling cash out, which creates taxable boot.

- Assuming the semiconductor-driven demand around Columbus applies to every submarket and asset class.

Start your Ohio 1031 exchange

Set up your exchange before your relinquished property closes, so the proceeds never reach your hands and the 45-day and 180-day clocks start clean. Contact our team to begin, or to talk through a specific deal.

Frequently asked questions

How much is capital gains tax on real estate in Ohio?

Ohio taxes the gain as ordinary income at roughly 2.75% to 3.5% for 2026 as it phases to a flat 2.75%, on top of federal capital gains tax.

Is there nonresident withholding when I sell Ohio property?

No. Ohio does not impose a general nonresident real estate withholding at closing.

Does Ohio conform to federal 1031 rules?

Yes. A properly structured exchange defers both the federal and the Ohio tax.

Do I need a qualified intermediary for an Ohio 1031 exchange?

Yes. The intermediary must hold the proceeds and facilitate the exchange. Engage one before the relinquished property closes.

This page is general information, not tax or legal advice. We act as a qualified intermediary and do not provide tax or legal advice. State and federal rules and thresholds change, and Ohio's rate is phasing down; confirm current figures with your tax advisor.

.jpg)

.jpg)

.jpg)