The "Silver Lining" of Disaster: How Section 1033 Offers What 1031 Cannot

No investor wants to lose a property to a wildfire, a hurricane, or an eminent domain seizure. It is a traumatic, chaotic financial event. But from a tax perspective, an "involuntary conversion" opens a door that is firmly locked to standard investors.

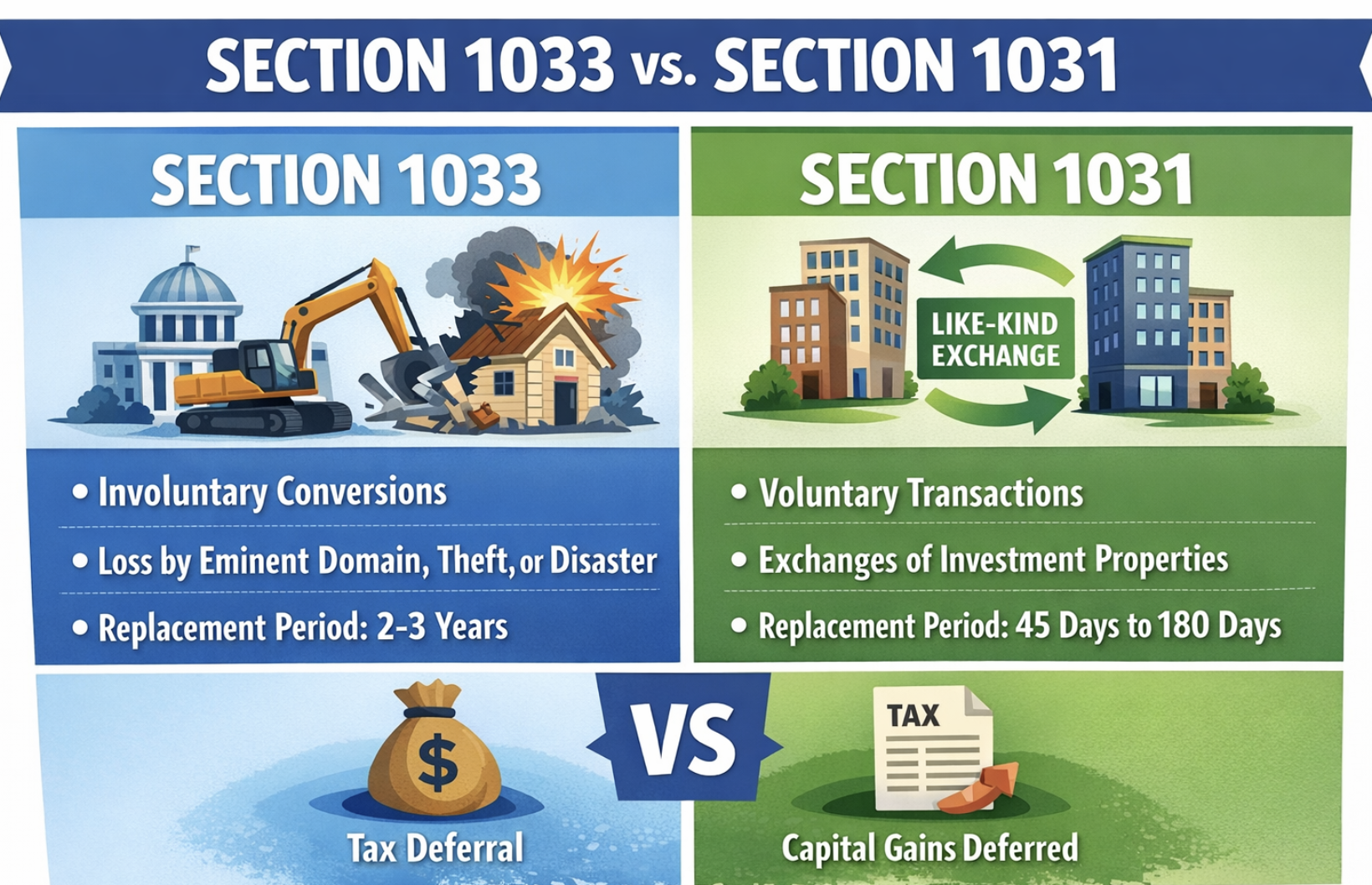

While the 1031 exchange is the famous tool for voluntary sales, Internal Revenue Code Section 1033 is its more powerful, more flexible, and less understood cousin.

In 2026, as climate-related disasters impact insurance payouts and infrastructure projects drive up eminent domain cases, understanding Section 1033 is no longer just for "worst-case scenarios"—it is essential portfolio defense.

The key difference? In a 1031 exchange, the IRS watches your every move with a stopwatch. In a 1033 exchange, the IRS gives you years to breathe, recover, and reinvest—often without a Qualified Intermediary touching your money.

This article details the critical differences between these two codes and how to maximize the "involuntary" advantage.

The Trigger: Voluntary vs. Involuntary

The primary distinction lies in intent.

- Section 1031: You chose to sell. Because it is voluntary, the rules are rigid. You have 45 days to identify a replacement and 180 days to close. You cannot touch the cash.

+2 - Section 1033: You were forced to sell. This includes:

- Destruction: Fire, flood, storm, or theft.

- Seizure: The government takes your property via eminent domain.

- Threat of Condemnation: You sell to the government (or a third party) because you have been notified that the government intends to seize it.

Because you didn't ask for this, the IRS offers you "grace."

The Three Massive Advantages of Section 1033

If you qualify for Section 1033 treatment, you gain three superpowers that a 1031 investor would kill for.

1. You Control the Cash (No QI Required)

In a 1031 exchange, if you touch one cent of the sales proceeds, the tax shield is broken. You must use a Qualified Intermediary (QI).

In a 1033 exchange, you do not need a QI. When the insurance company sends you a check for $2 million to cover your burnt-down apartment complex, you can deposit that check into your personal checking account. You can use the money to pay off personal debts, buy a boat, or invest in stocks—temporarily. As long as you purchase a qualifying replacement property within the statutory time limit, the tax deferral is valid.

2. The Extended Timeline

Forget the 45-day identification clock. It doesn't exist here.

- Standard Rule (Destruction/Theft): You have 2 years from the end of the tax year in which the gain was realized.

- Condemnation (Real Estate): You have 3 years from the end of the tax year.

- Federally Declared Disaster: If your property was in a Presidential Disaster Area (common for major hurricanes or wildfires), you have 4 years to reinvest.

Example: If your property burns down in August 2025 and you receive the insurance check in January 2026, your 2-year clock starts at the end of 2026. You have until December 31, 2028, to replace the property.

3. The "Equity Only" Rule (Debt Does Not Matter)

In a 1031 exchange, you must replace both the value and the debt (the "Equal or Greater" rule).

In a 1033 exchange, you only need to reinvest the amount of the proceeds received (equity). The IRS does not care if you get a new mortgage. If you receive a $1 million insurance check, you just need to buy a $1 million property. You do not need to replace the old mortgage that was paid off.

The Trap: "Similar Use" vs. "Like-Kind"

This is where Section 1033 can bite you. The standard for replacement property depends entirely on how you lost the property.

Scenario A: Destruction (Fire/Storm)

If your property is destroyed, the replacement property must be "Similar or Related in Service or Use."

- This is a stricter test than "Like-Kind."

- If you lost a hotel, you must buy another hotel. You cannot buy an apartment building.

- If you lost a warehouse used for your business, you cannot buy a retail strip center to rent out.

- Exception: If you were an investor (lessor) and not a user, the IRS is more lenient. If you rented out the warehouse, you can buy a retail center to rent out, because your "use" (collecting rent) is similar.

Scenario B: Seizure (Condemnation)

If your property is seized or sold under threat of condemnation, the IRS allows the broader "Like-Kind" standard (Section 1033(g)).

- You can replace seized raw land with an office building.

- You can replace a seized retail store with a multi-family complex.

- This is the "sweet spot" of Section 1033: You get the Like-Kind flexibility plus the 3-year timeline plus possession of your cash.

The "Threat of Condemnation" Loophole

You do not have to wait for the government to drag you to court to qualify for Section 1033.

If a government official (verbally or in writing) tells you, "We are planning to widen this highway and your building is in the way; we will take it if you don't sell," you are under Threat of Condemnation.

If you then turn around and sell that property to a private developer (who plans to deal with the government later), that sale still qualifies for Section 1033. You effectively get a "free pass" to do a 1033 exchange without a QI, just because the threat existed.

- Documentation is key: You must keep written records of the threat, news articles, or meeting minutes from the city council.

People Also Ask (FAQ)

Can I use Section 1033 for my primary residence? Yes. While Section 121 (the $250k/$500k exclusion) usually covers primary homes, Section 1033 is vital if your gain exceeds those limits. If your uninsured mansion burns down, you can use Section 1033 to defer the gain on the land value and insurance proceeds that exceed the $500k exclusion.

What if I can't find a property within 2 years? You can apply for an extension. Unlike the 1031 exchange, where deadlines are set in stone, the IRS has the discretion to grant extensions for Section 1033 if you can show "reasonable cause" (e.g., zoning delays, construction shortages).

Do I have to identify the replacement property to the IRS? No. There is no formal "45-day identification" form to file. You "identify" the property simply by buying it and reporting it on your tax return for that year.

What happens if I spend the insurance money and can't reinvest? If you spend the cash and fail to replace the property within the deadline, you must go back and amend your tax return for the year you received the money. You will owe the back taxes plus interest.

Final Thoughts: Don't Rush to 1031

In the wake of a disaster, many investors panic. They call a Qualified Intermediary and rush to set up a standard 1031 exchange, unwittingly locking themselves into a 45-day deadline and paying unnecessary fees.

Key Takeaway: If your property was taken or destroyed, stop. Do not open a 1031 exchange. Confirm your eligibility for Section 1033. You likely have years, not days, to make your next move, and you can keep the cash in your own pocket while you wait for the right deal.