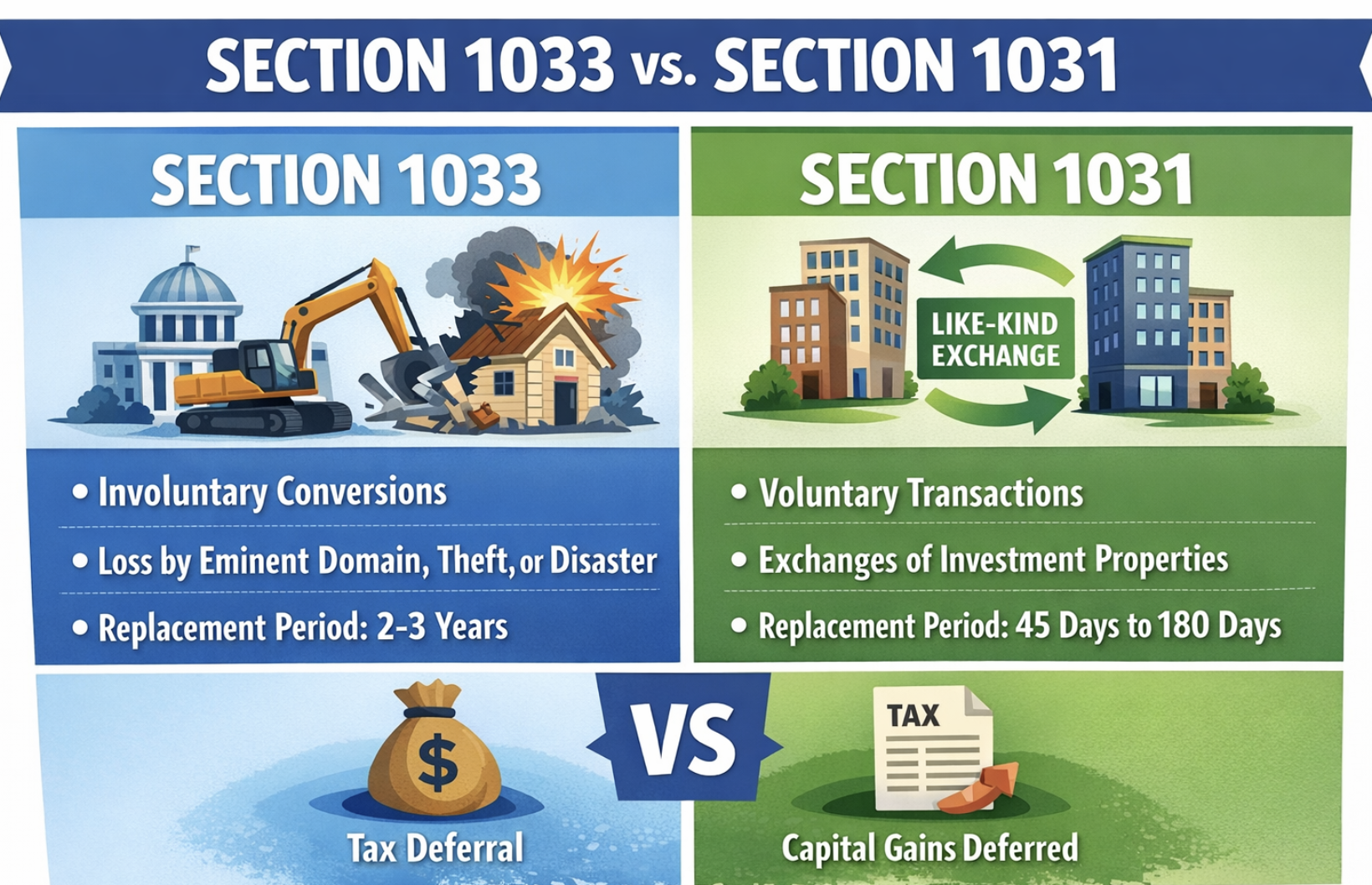

A 1031 exchange in Florida lets real estate investors sell an investment property and reinvest in like-kind property while deferring the tax on the gain. The exchange rules are federal and identical everywhere. What sets Florida apart is that there is no state income tax, so the only tax a Florida exchange defers is federal, and that Florida is the country's leading destination for both out-of-state and foreign real estate capital, which raises issues that rarely come up elsewhere. We act as your qualified intermediary, holding the proceeds and handling the documentation so the exchange stays valid from sale to closing.

Table of contents

- Is there a capital gains tax on real estate in Florida?

- FIRPTA: the issue that defines many Florida exchanges

- Florida 1031 exchange rules and timeline

- A caution for second-home owners

- Replacement-property math in Florida: insurance and property tax

- 1031 exchanges across Florida markets

- Common Florida 1031 exchange mistakes

- Start your Florida 1031 exchange

- Frequently asked questions

Is there a capital gains tax on real estate in Florida?

No. Florida has no state income tax, so there is no state capital gains tax on a property sale and no state withholding at closing, for residents and non-residents alike. The tax you defer in a Florida 1031 is entirely federal:

- Long-term capital gains at 0%, 15%, or 20%, with the 20% rate applying above $545,500 of taxable income for single filers and $613,700 for married couples filing jointly in 2026.

- The 3.8% Net Investment Income Tax above $200,000 of modified adjusted gross income for single filers, $250,000 for married couples.

- Depreciation recapture, taxed as unrecaptured Section 1250 gain at up to 25%.

A properly structured Florida exchange defers all of it. The full federal framework, the 45-day and 180-day deadlines and the qualified intermediary requirement, is in our main 1031 exchange guide.

FIRPTA: the issue that defines many Florida exchanges

Florida draws more foreign real estate investment than any other state, from Latin America, Canada, and Europe, so a federal withholding rule that barely registers elsewhere is central here. Under FIRPTA, when the seller is a foreign person, the buyer must generally withhold 15% of the gross sale price at closing and remit it to the IRS, regardless of the fact that Florida itself withholds nothing.

A foreign seller can still use a 1031, but FIRPTA does not switch off automatically. You apply for a withholding certificate so the IRS recognizes the deferral, and that application has to be coordinated with the exchange and its deadlines. Get the timing wrong and the buyer is still required to withhold 15%, which can strand the cash the exchange needs. If you are a foreign investor exchanging Florida property, the FIRPTA piece is the part to plan first.

Florida 1031 exchange rules and timeline

The federal rules govern, and the deadlines are strict:

- 45-day identification. Identify replacement property in writing within 45 days of the sale.

- 180-day closing. Close within 180 days of the sale, or by your return due date including extensions, whichever is earlier.

- No constructive receipt. Proceeds go to your qualified intermediary, never to you.

- Equal or greater value and debt. Reinvest all net proceeds and match or exceed the relinquished value and debt, or the shortfall is taxable boot.

- Same taxpayer. The entity that sold must be the entity that buys.

A caution for second-home owners

Florida is full of vacation and second homes, and many owners assume they can roll one into a 1031. They usually cannot. A 1031 requires property held for investment or business use, so a second home used personally does not qualify. It can qualify only with genuine, documented rental use and limited personal use, under the IRS safe harbor. If your Florida property is a personal getaway rather than a rental, talk through the facts before you assume an exchange is available.

Replacement-property math in Florida: insurance and property tax

Two Florida-specific costs belong in your underwriting, because they can move the after-tax yield more than the tax saving does.

Insurance is the first. Florida property insurance, particularly windstorm and flood coverage in coastal counties, has risen sharply and is now a major line item that can make or break a deal's cash flow. Underwrite it at current quotes, not last cycle's numbers.

Property tax is the second. Florida's effective property tax rate is moderate, but the homestead protections that cap increases apply only to a Florida primary residence, not to investment property. A 1031 replacement property is non-homestead, assessed at market and reassessed when you buy, with annual assessment increases capped at 10% rather than the 3% homestead cap. So the tax on a replacement deal resets to your purchase price and is not shielded the way an owner-occupied home is.

1031 exchanges across Florida markets

Miami and South Florida anchor the state's exchange activity and its international capital, in condominium, multifamily, and commercial property. Orlando draws tourism-driven and build-to-rent demand. Tampa Bay has been one of the fastest-growing metros in the country, strong in multifamily and industrial. Jacksonville offers logistics and lower entry prices, and Southwest Florida around Naples and Fort Myers carries second-home and investment demand. A large share of buyers here are reinvesting out of high-tax states, most often New York, New Jersey, and California, following the same migration as residents. Our New York to Florida and California guides cover those corridors.

Common Florida 1031 exchange mistakes

- Assuming no Florida tax means no withholding at all. A foreign seller still faces FIRPTA's 15% federal withholding, which has to be managed with a withholding certificate.

- Trying to exchange a personal second home that lacks genuine rental use.

- Underwriting a replacement deal on last year's insurance numbers in a coastal county.

- Taking receipt of the proceeds, even briefly, which disqualifies the exchange.

- Missing the 45-day identification window, or trading down into taxable boot.

Start your Florida 1031 exchange

Set up your exchange before your relinquished property closes, so the proceeds never reach your hands and, if you are a foreign seller, the FIRPTA certificate is underway. Contact our team to begin, or to talk through a specific deal.

Frequently asked questions

Does Florida have a capital gains tax on real estate?

No. Florida has no state income tax, so there is no state capital gains tax and no state withholding on a sale. Federal capital gains tax still applies.

Can a foreign investor do a 1031 exchange in Florida?

Yes. The exchange rules are the same, but FIRPTA's 15% federal withholding applies to foreign sellers and has to be handled with a withholding certificate so it does not break the exchange.

Can I 1031 my Florida vacation home?

Only if it is held for investment with genuine rental use and limited personal use. A second home used personally does not qualify for a 1031.

Do I still pay federal tax on a Florida 1031?

A 1031 defers federal capital gains, the Net Investment Income Tax, and depreciation recapture. It does not eliminate them; the deferred liability carries into the replacement property's basis.

Can I do a 1031 exchange from New York or California into Florida?

Yes, and it is common. The exchange defers your federal and origin-state tax. Florida adds no state tax on future income or the eventual sale, though your origin state may still reach the gain that accrued there on a later taxable sale.

This page is general information, not tax or legal advice. We act as a qualified intermediary and do not provide tax or legal advice. Federal rules and thresholds change; confirm current figures with your tax advisor.