Understanding the Basics of 1031 and 1035 Exchanges

A 1031 exchange and a 1035 exchange are both tax-deferred exchanges that allow individuals to swap one type of property for another, while deferring the payment of capital gains taxes. However, these exchanges have distinct purposes and benefits.

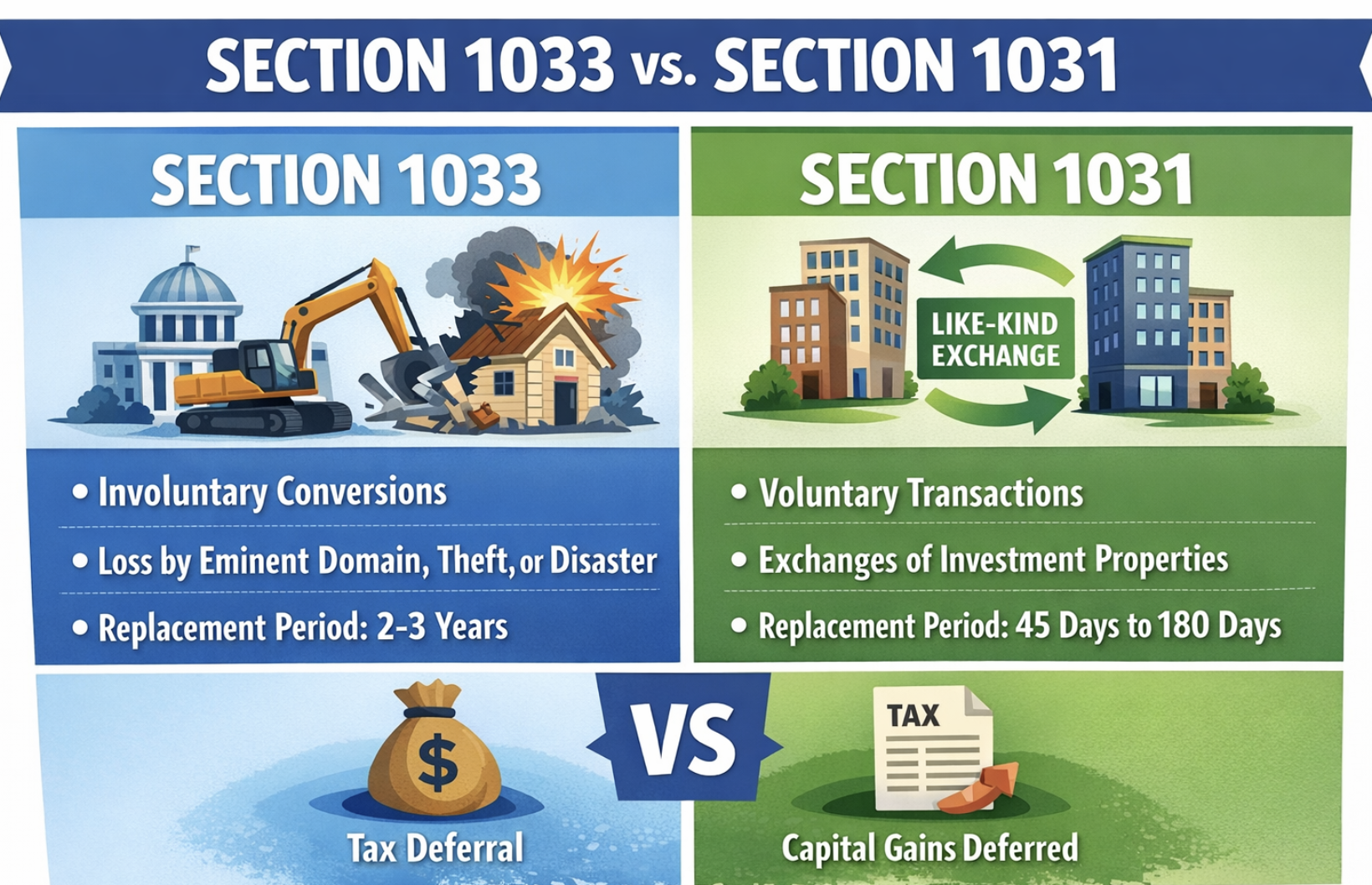

A 1031 exchange is commonly used in real estate transactions, where an investor can sell a property and use the proceeds to purchase a like-kind property, without incurring immediate capital gains taxes. This type of exchange is often utilized by investors looking to defer taxes and reinvest their profits into a new property, thereby maximizing their investment potential.

On the other hand, a 1035 exchange is specific to the insurance industry. It allows policyholders to exchange one insurance policy for another, without triggering any tax consequences. This type of exchange is commonly used by individuals who want to switch insurance providers or policies, while maintaining the tax-deferred status of their investment.

The Purpose and Benefits of 1031 Exchanges

A 1031 exchange, also known as a like-kind exchange, is primarily used for real estate investments. This exchange allows investors to sell a property and use the proceeds to acquire another similar property without incurring immediate capital gains taxes. By deferring the taxes, investors can reinvest more money into higher-value properties, expanding their real estate portfolios. The key benefit of a 1031 exchange is the ability to preserve wealth and defer taxes while maintaining or upgrading property investments.

Exploring the Advantages of 1035 Exchanges

Unlike a 1031 exchange, a 1035 exchange is specifically designed for insurance and annuity products. It allows individuals to exchange one insurance policy or annuity contract for another similar policy or contract without triggering immediate tax liabilities. This exchange is particularly beneficial for those who want to change insurance providers, update their coverage, or restructure their investment portfolios. The primary advantage of a 1035 exchange is the ability to switch insurance contracts or annuities without incurring tax consequences.

Key Differences Between 1031 and 1035 Exchanges

While both exchanges provide tax deferral benefits, there are important distinctions between them. The most significant difference lies in the types of assets eligible for exchange. 1031 exchanges are limited to real property, such as land, buildings, and rental properties. On the other hand, 1035 exchanges focus on insurance policies and annuity contracts, allowing for flexibility in the types of assets that can be exchanged.

Another key difference involves the time frames for completing the exchanges. In a 1031 exchange, there are specific deadlines that must be met to identify and acquire replacement properties, typically within 45 days and 180 days, respectively. In contrast, 1035 exchanges do not have strict timeframes and can be completed at any time, as long as the requirements for eligibility are met.

Eligible Properties for 1031 Exchanges vs. 1035 Exchanges

As mentioned earlier, 1031 exchanges are limited to real property, allowing investors to exchange one investment property for another. The properties exchanged must be similar or "like-kind," meaning they share the same nature, character, or class. For example, an investor can exchange a residential rental property for another residential rental property or a commercial property for another commercial property.

On the other hand, 1035 exchanges are applicable to insurance policies and annuity contracts. These policies and contracts can involve life insurance, endowment contracts, long-term care insurance, and various annuity products. It is important to consult with a qualified insurance professional to determine the eligibility of specific policies or contracts for a 1035 exchange.

How to Qualify for a 1031 Exchange: Rules and Regulations

To qualify for a 1031 exchange and defer capital gains taxes, certain requirements must be met:

1. Both the relinquished property (property sold) and the replacement property (property acquired) must be held for productive use in a trade or business or for investment purposes.

2. The properties involved in the exchange must be "like-kind," meaning they share the same nature or character.

3. The total purchase price of the replacement property or properties must be equal to or greater than the net sales price of the relinquished property.

4. The identification of the replacement property must be made within 45 days of the sale of the relinquished property. The acquisition of the replacement property should be completed within 180 days or by the due date of the tax return, including extensions, whichever is earlier.

5. Qualified intermediaries (QIs) must be involved to facilitate the exchange process and hold the funds during the transaction.

Requirements for a Successful 1035 Exchange: What You Need to Know

While the rules and regulations for a 1035 exchange are generally less strict than those of a 1031 exchange, there are still specific requirements to fulfill:

1. The exchange must involve insurance policies or annuity contracts that qualify for a 1035 exchange. Not all policies or contracts will meet the criteria, so it is essential to consult with an insurance professional to ensure eligibility.

2. The exchange must be made directly from one policy or contract to another. Cash withdrawals or surrendering the existing policy without acquiring a new one will not qualify for a 1035 exchange.

3. The policyholder must comply with the guidelines set forth by the insurance company and any applicable state laws regarding exchanges.

4. The exchange typically needs to occur within the same insurance company. However, there are circumstances where exchanges between different insurance companies can be allowed, such as when one company no longer offers the desired policy or when a company becomes insolvent.

Tax Implications of 1031 vs. 1035 Exchanges: A Comprehensive Overview

When it comes to tax implications, both 1031 and 1035 exchanges offer advantages but have different considerations:

1. 1031 exchanges provide the benefit of deferring capital gains taxes. By reinvesting the proceeds into a similar property, investors can continue to grow their investment portfolio without immediate tax consequences. However, it's important to note that the tax liability is not eliminated but deferred until a future taxable event occurs, such as the sale of the replacement property.

2. In contrast, 1035 exchanges are unique to insurance policies and annuity contracts. The primary tax advantage is the preservation of the policy's tax-deferred status. By exchanging one insurance policy or contract for another, the policyholder can maintain the tax advantages and postpone taxable events associated with distributions or withdrawals.

Individuals considering either type of exchange should consult with tax professionals to understand the specific tax implications and plan accordingly.

Timing Considerations for a Smooth 1031 or 1035 Exchange Process

Timing is crucial when executing a 1031 or 1035 exchange:

1. For a 1031 exchange, the identification of replacement properties must be made within 45 days from the sale of the relinquished property. It is essential to thoroughly research and evaluate potential replacement properties within this timeframe to make informed investment decisions.

2. The acquisition of the replacement property or properties must be completed within 180 days from the sale of the relinquished property or by the due date of the tax return, including extensions, whichever is earlier. Proper planning and coordination with all parties involved, including qualified intermediaries and real estate professionals, are necessary to ensure a smooth and timely exchange process.

3. In the case of a 1035 exchange, the timing is more flexible, as there are no strict deadlines. However, individuals should consider the policy's terms and any potential penalties associated with surrendering or terminating the existing policy before initiating an exchange.

Common Pitfalls to Avoid in a 1031 or 1035 Exchange Transaction

While 1031 and 1035 exchanges offer substantial benefits, there are common pitfalls that individuals should be aware of to navigate the process successfully:

1. Failing to meet the strict timelines and deadlines associated with a 1031 exchange can result in disqualification and immediate tax liabilities. It is crucial to stay organized and adhere to the requirements for identification and acquisition of replacement properties within the specified timeframes.

2. In a 1035 exchange, individuals may encounter surrender charges or fees associated with the termination of an existing insurance policy or annuity contract. It is essential to review the terms of the policies or contracts to understand potential financial implications before initiating an exchange.

3. Not seeking professional advice can lead to costly mistakes. Engaging the expertise of qualified intermediaries, real estate professionals, and insurance advisors can help ensure compliance with regulations, maximize the benefits of the exchanges, and minimize potential risks.

Real-Life Examples: Case Studies of Successful 1031 and 1035 Exchanges

Real-life case studies provide practical insights into the successful execution of 1031 and 1035 exchanges. These examples demonstrate how individuals have utilized the exchanges to achieve their investment and financial goals. They showcase the diverse scenarios in which 1031 and 1035 exchanges can be applied, offering inspiration and guidance for those considering similar exchanges.

Expert Tips and Strategies for Maximizing the Benefits of a Like-Kind Exchange

Experts in tax planning and real estate investment provide valuable tips and strategies for maximizing the benefits of a like-kind exchange:

1. Carefully consider the timing of the exchange to align with appreciation in property value, potential tax law changes, and market conditions.

2. Consult with financial advisors, real estate professionals, and tax planners to ensure compliance with regulations and identify suitable replacement properties or policies.

3. Thoroughly research and evaluate potential replacement properties or policies to make informed investment decisions and mitigate risks.

4. Use professional appraisals and property valuations to determine fair market values, especially in situations where the properties exchanged may have differing values.

How to Navigate Complexities in a 1031 or 1035 Exchange: Practical Advice

Navigating the complexities of a 1031 or 1035 exchange requires careful planning and practical advice:

1. Maintain comprehensive records throughout the exchange process. This includes records of property or policy valuations, correspondence with qualified intermediaries, and any relevant documentation that demonstrates compliance with regulations.

2. Familiarize yourself with the IRS guidelines and regulations governing 1031 and 1035 exchanges. Periodically review these guidelines, as they may change over time.

3. Seek professional advice from tax experts, insurance professionals, or attorneys who specialize in exchange transactions. They can provide valuable insights and ensure compliance with complex rules and regulations.

The Role of Qualified Intermediaries in Facilitating Smooth Exchange Transactions

Qualified intermediaries (QIs) play a vital role in facilitating smooth exchange transactions:

1. QIs are independent third parties who assist in structuring and administering 1031 and 1035 exchanges. They hold funds during the transaction to ensure compliance with IRS rules and regulations.

2. The involvement of a QI is crucial to meeting the requirements and timelines set forth in the exchange process. They help navigate the technical aspects of the exchange, oversee the transfer of properties or policies, and safeguard funds to prevent immediate tax consequences.

3. It is essential to select a reputable and experienced QI who has a thorough understanding of exchange transactions and compliance with IRS guidelines. Their expertise and guidance can significantly streamline the exchange process and mitigate potential risks.

Exploring Alternative Options to Consider Instead of a Like-Kind Exchange

While 1031 and 1035 exchanges offer significant benefits, there are alternative options to consider:

1. For individuals looking to diversify their investments or reduce management responsibilities, real estate investment trusts (REITs) can provide a passive investment option without the requirement of owning or managing physical properties.

2. Partial exchanges allow individuals to exchange only a portion of their property or policy, providing flexibility while still enjoying the tax deferral benefits.

3. Tax-advantaged investment vehicles, such as qualified opportunity zones (QOZs) or Section 721 exchanges, offer alternative ways to defer capital gains taxes.

It is crucial to evaluate and discuss these alternatives with qualified professionals to determine the most suitable strategy based on individual circumstances and investment objectives.

Potential Challenges and Risks Associated with Both Types of Exchanges

While 1031 and 1035 exchanges offer significant benefits, there are potential challenges and risks to be aware of:

1. In both types of exchanges, finding suitable replacement properties or policies within the specified timeframes can be challenging. Proper due diligence, market research, and assistance from real estate professionals or insurance advisors can help mitigate this risk.

2. Changes in tax laws and regulations can impact the benefits and eligibility of exchanges. Staying informed about tax rules and consulting with tax professionals can help navigate these potential challenges.

3. Both types of exchanges involve additional administrative steps, such as coordinating with qualified intermediaries, insurance companies, or other professionals. Proper planning and timely execution are necessary to ensure a smooth transaction.

Understanding the Impact of Recent Tax Law Changes on 1031 and 1035 Exchanges

It is important to stay informed about recent tax law changes that may impact 1031 and 1035 exchanges:

1. Tax laws are subject to change, and revisions may affect the eligibility, rules, and tax benefits associated with these exchanges. Consultation with tax professionals and staying updated with current tax legislation is crucial when considering 1031 or 1035 exchanges.

2. Changes in capital gains tax rates or the elimination of certain tax deductions may influence the financial implications of these exchanges. Understanding the potential impact on one's financial situation and consulting with professionals can help make informed decisions.

By comprehensively analyzing the similarities, differences, benefits, eligibility requirements, and potential risks associated with 1031 and 1035 exchanges, individuals can make informed decisions regarding their investment and insurance strategies. Consultation with qualified professionals and thorough research are essential to ensure compliance with regulations and maximize the advantages of these exchange options.

Q: What are the key differences between 1031 and 1035 exchanges for an investor?

A: The primary differences involve the assets covered and specific rules. A 1031 exchange, defined under section 1031 of the internal revenue code, allows investors to defer capital gains tax when exchanging real property held for business or investment purposes for other "like-kind" real estate. A 1035 exchange is specific to insurance products, allowing tax-free exchanges between life insurance policies, annuities, and endowment contracts. While both offer tax deferral benefits, 1031 exchanges involve real estate properties, whereas 1035 exchanges involve insurance or annuities products.

Q: How does tax deferral work differently in 1035 and 1031 exchanges?

A: In a 1031 exchange, the tax deferral applies to capital gains tax on real estate used for business or investment purposes. The investor can postpone recognition of gain or loss as long as they reinvest in property of equal or greater value. In a 1035 exchange, the tax deferral applies to any built-up gains in life insurance policies or annuities, allowing policyholders to transfer from one insurance product to another without triggering taxable events. Both are powerful tax strategies regulated by the internal revenue service, but they apply to completely different asset classes.

Q: What types of properties qualify for 1031 exchanges?

A: Under section 1031 of the internal revenue code, only real property held for productive use in business or held for investment qualifies for 1031 exchange treatment. This includes commercial buildings, rental properties, vacant land, farmland, and investment real estate. Property used primarily as a personal residence does not qualify. Additionally, the replacement property must be of "like-kind" to the relinquished property, though this is broadly interpreted for real estate. Real estate investors to defer capital gains must ensure both properties are held for business or investment purposes rather than primarily for personal use or resale.

Q: Can an investor exchange life insurance policies under a 1031 exchange?

A: No, an investor cannot exchange life insurance policies under a 1031 exchange. Section 1031 of the internal revenue code applies exclusively to real property held for business or investment purposes. To exchange life insurance policies, annuities, or endowment contracts tax-free, investors must use a 1035 exchange instead. Section 1035 was specifically designed for life insurance and annuity exchanges. It's important to consult with a qualified tax advisor before proceeding with either type of exchange to ensure compliance with the internal revenue service regulations.

Q: What are the time constraints for completing 1031 vs 1035 exchanges?

A: 1031 exchanges have strict time constraints: investors must identify potential replacement properties within 45 days of selling the relinquished property and must complete the exchange within 180 days. These deadlines are strictly enforced by the internal revenue service. In contrast, 1035 exchanges for insurance products have no specific time limits. You can exchange a life insurance policy or annuity for another qualifying contract at any time, as long as the requirements for a direct transfer are met. This timing flexibility is one of the advantages of 1035 exchanges compared to the rigid deadlines of 1031 exchanges.

Q: How can 1035 and 1031 exchanges be used in estate planning?

A: Both exchanges offer valuable estate planning benefits. A 1031 exchange allows real estate investors to defer capital gains taxes while building wealth through investment real estate, potentially passing appreciated properties to heirs who may receive a stepped-up basis upon inheritance. A 1035 exchange can be used to update life insurance policies to ones with better benefits or more favorable terms without tax consequences, ensuring estate liquidity. Both strategies can preserve wealth by minimizing tax liabilities, though they address different aspects of estate planning. Consultation with a tax advisor is essential to determine how these exchanges can be integrated into a comprehensive estate planning strategy.

Q: Is there a limit on the number of 1031 or 1035 exchanges an investor can complete?

A: There is no limit on the number of properly structured 1031 or 1035 exchanges an investor can complete over their lifetime. An investor can conduct sequential 1031 exchanges with investment real estate, continually deferring capital gains taxes as long as each exchange meets the requirements under section 1031 of the internal revenue code. Similarly, there's no restriction on how many times an individual can exchange life insurance policies or annuities under section 1035. However, frequent exchanges might attract scrutiny from the internal revenue service, so it's advisable to have legitimate business or investment purposes for each transaction.

Q: What are the potential pitfalls when executing 1031 and 1035 exchanges?

A: For 1031 exchanges, common pitfalls include missing strict deadlines, incorrect property identification, receiving "boot" (non-like-kind property or cash that triggers partial taxation), or exchanging properties not held for investment. For 1035 exchanges, pitfalls include surrendering the old policy before the new one is in force, exchanging to a policy with less income potential, or making exchanges that don't qualify under section 1035. Both types of exchanges require careful adherence to specific rules and typically involve qualified intermediaries or insurance carriers to facilitate the process. Consulting with a tax advisor before initiating either exchange is crucial to avoid these potential issues.

Q: How does basis calculation differ between 1031 and 1035 exchanges?

A: In a 1031 exchange, the tax basis of the relinquished property transfers to the replacement property, potentially adjusted for additional investment or received boot. This means the original acquisition date and depreciation schedule generally carry over. In a 1035 exchange, the cost basis of the original life insurance policy or annuity transfers to the new contract. However, there are important distinctions in how policy loans, surrender charges, and premiums affect basis in insurance exchanges. Both exchanges essentially preserve the tax position from the original asset, deferring recognition of gain or loss until the replacement property or policy is ultimately sold or surrendered without being part of another qualifying exchange.

.jpg)