In the realm of real estate investing, utilizing a 1031 exchange can be an advantageous strategy for those looking to defer capital gains taxes on the sale of a property. When it comes to the specific niche of raw land investments, understanding the regulatory landscape is crucial for maximizing the benefits of a 1031 exchange. This article aims to provide a comprehensive exploration of the regulations and considerations involved in such transactions.

Understanding the Basics of 1031 Exchanges

A 1031 exchange, also known as a like-kind exchange, allows real estate investors to defer capital gains taxes when they sell a property and use the proceeds to acquire a replacement property. This strategy is authorized under Section 1031 of the Internal Revenue Code.

One key requirement of a 1031 exchange is that the properties involved must be of "like-kind." Generally, this means that the properties must be of the same nature or character, such as raw land for raw land or a commercial building for another commercial building.

By deferring capital gains taxes, investors have the opportunity to reinvest their funds into potentially more lucrative properties without a tax burden. However, it is important to understand the specific regulations and considerations when incorporating raw land investments into a 1031 exchange.

When incorporating raw land investments into a 1031 exchange, there are a few important factors to consider. Firstly, the land must be held for investment or business purposes, rather than for personal use. Additionally, the land must be located within the United States, as foreign properties do not qualify for a 1031 exchange.

Furthermore, it is crucial to be aware of the strict timeline associated with a 1031 exchange. Once the initial property is sold, the investor has 45 days to identify potential replacement properties and 180 days to complete the acquisition of the replacement property. Failure to meet these deadlines can result in the disqualification of the exchange and the imposition of capital gains taxes.

Lastly, it is highly recommended to consult with a qualified tax advisor or real estate professional who specializes in 1031 exchanges. They can provide guidance on the specific rules and regulations that apply to raw land investments and ensure compliance with all requirements.

The Benefits of Investing in Raw Land

Raw land investments offer unique advantages for real estate investors. Unlike developed properties, raw land does not require ongoing maintenance or improvements, making it a relatively hands-off investment.

Moreover, raw land provides investors with the opportunity to be creative and tailor their development plans according to market demands. It can be utilized for various purposes such as residential, agricultural, or recreational purposes, depending on zoning regulations and market conditions.

Additionally, the potential for appreciation is often higher for raw land compared to developed properties. As areas undergo urbanization or experience population growth, the demand for land can increase significantly, leading to attractive returns for investors.

Exploring the Potential of Raw Land Investments

When considering raw land investments within the context of a 1031 exchange, it is crucial to thoroughly assess the potential of the properties involved. Conducting comprehensive due diligence is key to mitigate risks and maximize returns.

Factors such as location, accessibility, zoning regulations, environmental considerations, and market trends must all be carefully evaluated. Is the land situated in a growing area with demand for development? Are there any restrictions or limitations on how the land can be used? Assessing these aspects will help determine the viability and potential return on investment.

Furthermore, investors should consider the long-term outlook for the property. Are there any planned infrastructure developments or upcoming zoning changes that could impact its value? Analyzing these potential catalysts can assist in making informed investment decisions.

How 1031 Exchanges Can Benefit Raw Land Investors

Raw land investors can leverage the benefits of a 1031 exchange to optimize their investment strategy. By deferring capital gains taxes, investors can allocate a larger portion of their funds towards the acquisition of higher-value raw land, potentially increasing their returns over time.

In addition to tax deferral, a 1031 exchange offers the opportunity for investors to diversify their real estate portfolio. Investors can exchange their raw land for other types of properties, such as commercial buildings or rental properties, further expanding their investment options.

Navigating the Regulatory Landscape of 1031 Exchanges and Raw Land Investments

While the benefits of incorporating raw land investments into a 1031 exchange are substantial, it is essential to navigate the regulatory landscape carefully. Compliance with specific rules and regulations is paramount to ensure a successful and legitimate exchange.

One critical regulation to consider is the strict timeline imposed for completing a 1031 exchange. From the date of sale of the relinquished property, investors have 45 days to identify potential replacement properties and 180 days to close on the selected property.

Additionally, there are rules regarding the use of qualified intermediaries (QIs) in 1031 exchanges. QIs play a crucial role in facilitating the exchange and ensuring compliance with IRS regulations. They hold the funds from the sale of the relinquished property until the purchase of the replacement property is completed.

Key Regulations to Consider Before Engaging in a 1031 Exchange with Raw Land

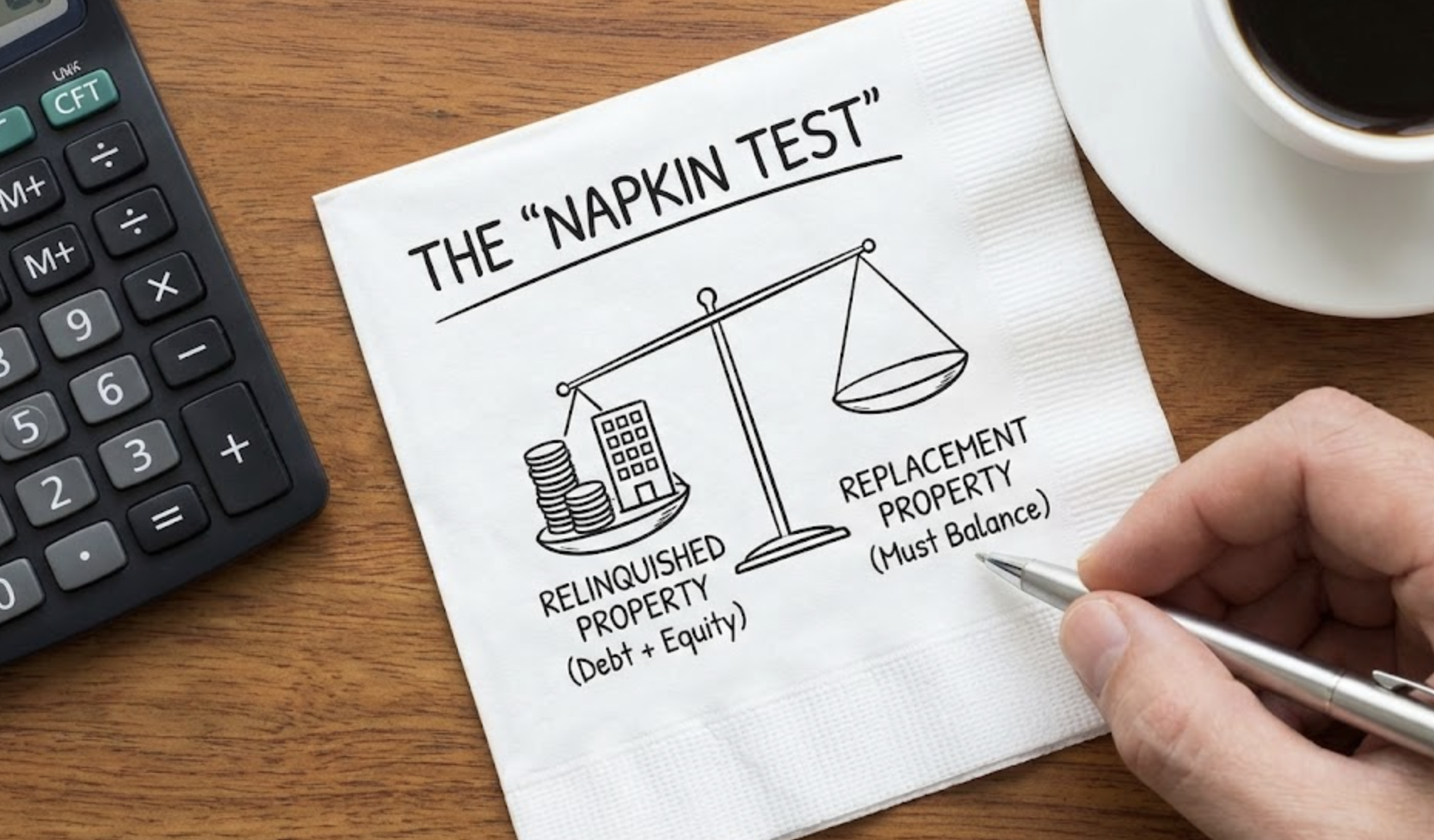

Before engaging in a 1031 exchange involving raw land, investors should be aware of various regulations that could affect the transaction. One essential requirement is the equal or greater value rule, which states that the investment in the replacement property must be of equal or greater value compared to the relinquished property.

In addition, the same taxpayer rule stipulates that the taxpayer who sells the relinquished property must be the same taxpayer who acquires the replacement property. This means the investor cannot sell a property as an individual and then purchase a replacement property under a different legal entity, such as a corporation or partnership.

Moreover, the properties involved in the exchange must be held for investment or use in a business, meaning they cannot be personal residences or vacation homes. Following these regulations is crucial to ensure the validity of the 1031 exchange and its tax benefits.

The Role of Qualified Intermediaries in 1031 Exchanges Involving Raw Land

Qualified intermediaries (QIs) are an indispensable element of a 1031 exchange involving raw land. Their involvement is crucial for maintaining compliance with IRS regulations and facilitating the smooth execution of the exchange process.

QIs act as trusted third parties who hold the funds from the sale of the relinquished property and disburse them for the purchase of the replacement property. This arrangement ensures that the investor does not have direct control or access to the funds during the exchange process, preventing the exchange from being invalidated.

Engaging the services of a reputable and experienced QI is essential. They have the expertise to guide investors through the entire process, ensuring compliance with the necessary regulations and maximizing the benefits of the 1031 exchange.

Tax Implications of 1031 Exchanges and Raw Land Investments

One of the primary advantages of a 1031 exchange is the deferral of capital gains taxes. By reinvesting the proceeds from the sale of the relinquished property into a replacement property, investors can postpone paying taxes on the gain until a future taxable event, such as selling the replacement property.

It's important to note that a 1031 exchange allows for the deferral of taxes, not the total elimination of tax liability. If an investor eventually sells the replacement property without utilizing a subsequent 1031 exchange, they will be responsible for paying the accrued capital gains taxes at that time.

Furthermore, investors should consult with tax professionals to fully understand the tax implications associated with a 1031 exchange involving raw land investments. Tax laws can be complex and subject to change, so seeking professional advice is crucial for accurate tax planning.

Strategies for Maximizing Tax Savings in a 1031 Exchange with Raw Land

While a 1031 exchange already provides significant tax savings, there are additional strategies that investors can employ to further maximize their tax advantages when exchanging raw land.

One common strategy is to pair a 1031 exchange with a conservation easement. A conservation easement is a voluntary agreement between a landowner and a qualified organization that restricts the future development or use of the land to protect its conservation value. By placing a conservation easement on the replacement property, the investor may be eligible for additional tax benefits, such as income tax deductions or property tax reductions.

Another strategy involves utilizing a Delaware Statutory Trust (DST) structure. A DST is a separate legal entity that owns and manages investment properties. By investing in a DST rather than directly holding the replacement property, investors can diversify their investment portfolio, potentially reduce management responsibilities, and enhance tax planning opportunities.

Common Mistakes to Avoid When Utilizing a 1031 Exchange for Raw Land Investments

While a 1031 exchange can be a powerful tool for deferring taxes and optimizing raw land investments, there are common pitfalls that investors should be mindful of to avoid costly mistakes.

One common mistake is failing to meet the strict timeline requirements for identifying and closing on replacement properties. Missing the 45-day identification window or the 180-day closing period can jeopardize the qualification of the exchange, resulting in the immediate tax liability on the capital gains.

Another mistake to avoid is disregarding the equal or greater value rule. Investing in a replacement property of lesser value can trigger partial recognition of capital gains, requiring the investor to pay taxes on the difference.

Additionally, not conducting thorough due diligence on potential replacement properties can lead to unfavorable investments. Failing to assess market conditions, growth potential, zoning regulations, or environmental considerations can result in purchasing a replacement property with limited or diminished value.

Case Studies: Successful 1031 Exchange Transactions with Raw Land Assets

Examining real-world examples can showcase the potential benefits and outcomes of successful 1031 exchange transactions involving raw land. Case studies illustrate how investors have utilized the strategies discussed above to maximize their investments and defer taxes.

These case studies can provide valuable insights into different scenarios, investment objectives, and the potential returns achievable through proper planning and execution. However, it is essential to recognize that each investment is unique, and outcomes may vary based on specific circumstances and market conditions.

Exploring Alternative Investment Options for Raw Land Investors Using a 1031 Exchange

While raw land investments offer attractive prospects for real estate investors, some may prefer to explore alternative investment options within the context of a 1031 exchange.

One alternative is investing in income-generating properties, such as residential or commercial real estate. These properties provide regular cash flow through rental income and may offer potential for appreciation over time.

Investing in a real estate investment trust (REIT) is another option. REITs are companies that own, operate, or finance income-generating real estate properties. By investing in REITs, investors can access a diversified portfolio of properties while benefiting from the potential returns associated with real estate investments.

Evaluating the Potential Risks and Rewards of Raw Land Investments in a 1031 Exchange Context

As with any investment, raw land investments within a 1031 exchange context come with their own set of risks and potential rewards. It is essential for investors to thoroughly evaluate these factors before making investment decisions.

One primary risk of raw land investments is the potential for limited liquidity. Unlike stocks or bonds, raw land can take longer to sell, especially in less-developed or less-desirable areas.

Market conditions can also impact an investor's potential return on investment. Economic downturns or changes in local market dynamics can affect the demand for raw land and considerably alter its value.

On the other hand, the rewards of raw land investments can be substantial. As previously mentioned, the potential for appreciation can be significant, particularly in areas experiencing population growth or urbanization. Moreover, the hands-off nature of raw land investments can provide investors with greater flexibility and less active management compared to developed properties.

How to Conduct Due Diligence on Raw Land Properties for a Successful 1031 Exchange

Conducting thorough due diligence on raw land properties is crucial for a successful 1031 exchange. Investors must evaluate multiple factors to ensure the viability and potential return of the investment.

Location is a fundamental consideration. Researching the area's economic growth, population trends, and development plans can provide insight into the potential value appreciation of the land.

Understanding zoning regulations and any potential restrictions on land use is equally important. Working with professionals, such as real estate attorneys or land use consultants, can help navigate these complexities and determine the feasibility and limitations of the land.

Conducting environmental assessments and surveys is essential to identify any potential issues or liabilities associated with the land. Assessing any existing or potential easements, restrictions, or encumbrances is crucial to avoid unforeseen complications.

In conclusion, a 1031 exchange provides real estate investors with the opportunity to defer capital gains taxes and expand their investment opportunities. When incorporating raw land investments into a 1031 exchange, understanding the regulatory landscape, conducting due diligence, and engaging qualified intermediaries are essential for maximizing the benefits and mitigating risks. Thoroughly examining all aspects and adhering to the appropriate regulations can help ensure a successful exchange and optimize returns for investors in the ever-growing realm of raw land investments.